Quarter season is upon us. At this point we want to look at the “extraordinary” figures in Volkswagen, BMW and Mercedes, and what the markets expect from the financial data in the short and long term.

Volkswagen, Mercedes and BMW: look at dividend yields and P/E ratios

Valuations are still hard to believe: At Volkswagen (quarterly figures on 30 April), investors who buy preferred shares are now given the prospect of a dividend yield of 7.57% for 2024 and 7.95% for 2025 – Of course, always taking into account the expected profit and Analysts will also be provided by Volkswagen. The P/E ratio (price earnings ratio) for 2024 is expected to be 3.95 and for 2025 3.68. You really have to describe it as very cheap! If this profit were to occur in this way and the Wolfsburg-based company were to distribute the full profit, the investor would recoup his share purchase price in no more than 4 years through profit distribution. A P/E ratio below 10 is considered very cheap. But a value below 4 is surprising.

At BMW, the date of the quarterly figures is still unclear. The expected dividend yield for this year and next year is 5.37% and 5.53%. The expected P/E ratio is 6.41% and 6.33%. Damn good data! And Mercedes (reported April 30) offers dividend yields of 6.65% and 6.84% over the next two years, according to market estimates, as well as strong P/E ratios of 6.3 and 6.

Current quarterly profit expectations

For the first quarter, which Volkswagen will report in two weeks, analysts expect average earnings per share of 7.58 euros. In the same quarter last year, 8.43 euros were reported. According to expectations, BMW expects earnings per share of 4.40 euros for the last three months, compared to 5.31 euros in the same quarter last year. For Mercedes, earnings per share are expected to be 2.61 euros, compared to 3.69 euros in the same quarter last year. You can see: For all three manufacturers, profits can decrease from year to year.

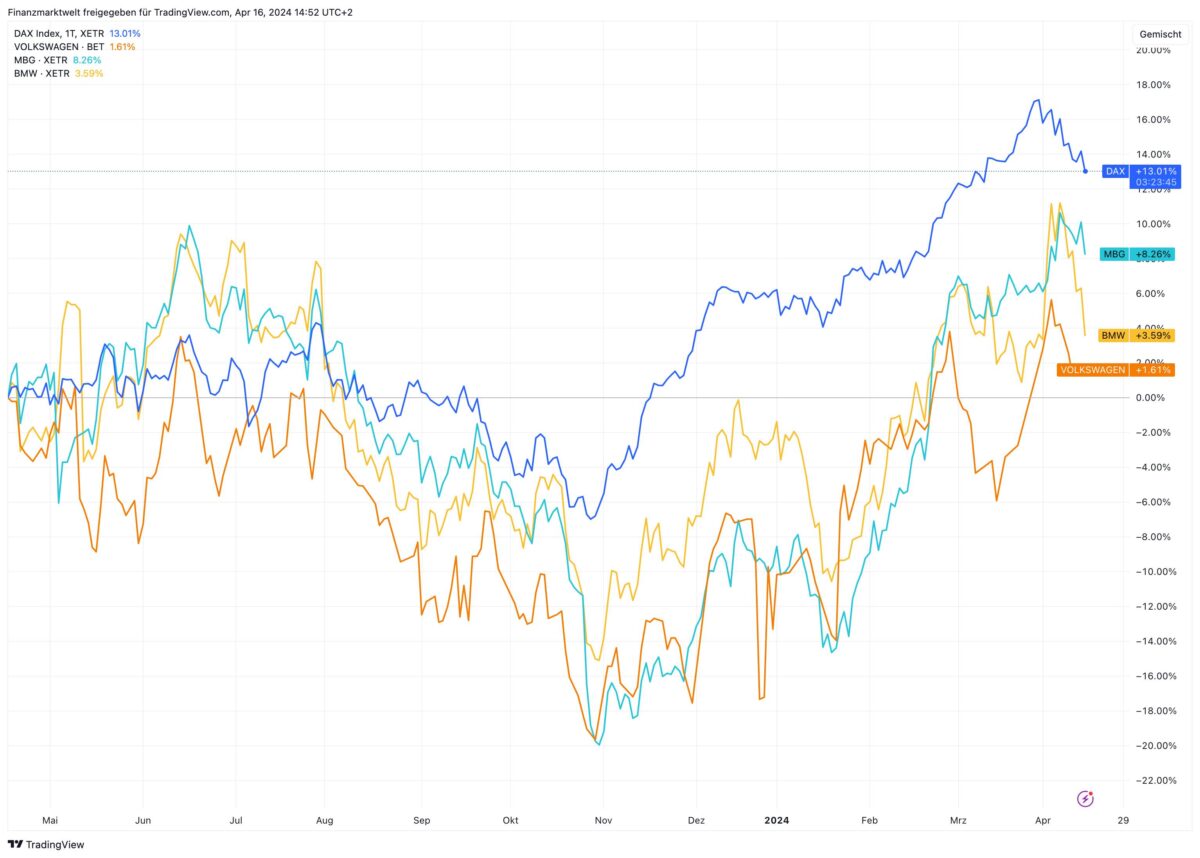

Stock performance

But because the automaker’s stock has performed so weakly, the average entry prices for new buyers of the stock provide a good balance between the stock and earnings per share. This chart shows the DAX compared to three stocks. In the last twelve months, the Dax rose by 13%, while Volkswagen only managed to gain 1.6% and BMW 3.6%. After all, Mercedes got 8.3%. But you can see that the performance of car manufacturers lagged behind the DAX.

Dividend distributions: a constant expectation

At Volkswagen, market expectations indicate that dividend payments for the next four years will remain constant at more than 9 euros per share. In BMW it will be more than 5 euros in dividends for the next two years and then more than 6 euros in dividends. At Mercedes, a dividend of 4.9 euros is expected for 2024, and more than 5 euros per share in the years after that. So the market expects not only good profits, but also continued high payouts, which are similar to the high yields of the division mentioned above.

Bayer as a warning example

But please always consider Bayer as a warning example! The company has been struggling for years with massive damage claims and lawsuits in the US over the weed killer Roundup, which is said to cause cancer. Bayer was able to maintain its dividend at a high level for a long time and therefore provide a high dividend yield. But then – without prior notice – Bayer announced on February 19 that it had reduced its dividend from 2.40 euros to 0.11 euros. This means that annual high dividend payments as a pain reliever for ever-declining stock prices are history, from now on.

Could this also happen to car manufacturers? It is not clear! But anyone who continues to believe that Volkswagen, Mercedes, BMW and Co will continue to make huge profits in the next few years and can overcome the challenges of weak demand for electric cars etc. will find entries with very good numbers. But as I said, Bayer’s example basically requires caution. After all, returns that are significantly higher than the market average always mean high risk – otherwise investors would buy these shares in such large quantities that the high price would reduce the profits for foreigners.

Risk warning: Trading securities and financial instruments can put your capital at greater risk, possibly even more than the capital invested. Marketing is not for everyone. Past performance is no guarantee of future performance. The analysis presented here does not constitute investment advice and therefore is not a recommendation to buy or sell securities, futures contracts or any other financial instrument. The analysis provided is intended for informational purposes only and cannot take the place of individual consultation. Liability for indirect and direct consequences from these recommendations is therefore excluded.

FMW and data from Bloomberg Terminal

Related posts:

2025 Audi A3 Elevates Compact Luxury with Cutting-Edge Technology

2025 Audi A3 Elevates Compact Luxury with Cutting-Edge Technology

Unveiling the 2025 Cadillac CT5-V Blackwing

Unveiling the 2025 Cadillac CT5-V Blackwing

Recall Issued for 147,110 Hyundai, Kia, and Genesis Electric Vehicles

Recall Issued for 147,110 Hyundai, Kia, and Genesis Electric Vehicles

2025 Cadillac Optiq Redefining Automotive Intelligence

2025 Cadillac Optiq Redefining Automotive Intelligence

2024 Jeep Gladiator Mojave Keeps On Thriving

2024 Jeep Gladiator Mojave Keeps On Thriving

Genesis GV60 Magma Signals the Arrival of a Dynamic Performance Brand

Genesis GV60 Magma Signals the Arrival of a Dynamic Performance Brand

2024 Chevrolet Equinox EV – Where Sustainability Meets Performance

2024 Chevrolet Equinox EV – Where Sustainability Meets Performance

2024 Alfa Romeo Tonale Shines with Stylish Sophistication

2024 Alfa Romeo Tonale Shines with Stylish Sophistication

2024 Honda CR-V Hybrid, Redefining Sustainable Driving in SUVs

2024 Honda CR-V Hybrid, Redefining Sustainable Driving in SUVs

Unveiling the 2025 Genesis GV80, Luxury and Innovation in SUV Design

Unveiling the 2025 Genesis GV80, Luxury and Innovation in SUV Design

2024 Alfa Romeo Stelvio Quadrifoglio Sets New Standards for SUV Performance

2024 Alfa Romeo Stelvio Quadrifoglio Sets New Standards for SUV Performance

2025 Acura ADX: A Compact SUV with Strong Civic and Integra Heritage

2025 Acura ADX: A Compact SUV with Strong Civic and Integra Heritage

2025 Fisker Alaska – Redefining Adventure with Electric Power

2025 Fisker Alaska – Redefining Adventure with Electric Power

Nikola’s HYLA Stations Signal Its Supercharger Moment

Nikola’s HYLA Stations Signal Its Supercharger Moment

2021 BMW i3 Continues to Lead the Way in Electric Mobility with Sustainable Innovation

2021 BMW i3 Continues to Lead the Way in Electric Mobility with Sustainable Innovation

Putting the 2024 Lexus GX550 to the Test in Its Element

Putting the 2024 Lexus GX550 to the Test in Its Element

2025 Audi Q4 e-tron and Q4 e-tron Sportback Lead the Charge in Electric SUV Innovation

2025 Audi Q4 e-tron and Q4 e-tron Sportback Lead the Charge in Electric SUV Innovation

2025 Hyundai Tucson Unveils Striking Mug and Desktop-Inspired Dash in U.S. Specification

2025 Hyundai Tucson Unveils Striking Mug and Desktop-Inspired Dash in U.S. Specification

All-New Renault Duster is Here to Dominate in 2024

All-New Renault Duster is Here to Dominate in 2024

Catching the Eclipse in the Upcoming Generation of Toyota 4Runner

Catching the Eclipse in the Upcoming Generation of Toyota 4Runner

2024 Fiat 500e – Redefining Urban Mobility with Style

2024 Fiat 500e – Redefining Urban Mobility with Style

Testing the 2024 Lexus UX250h, Your City Sipper Companion

Testing the 2024 Lexus UX250h, Your City Sipper Companion

2024 Chrysler Pacifica – Elevating Comfort and Versatility

2024 Chrysler Pacifica – Elevating Comfort and Versatility

Unveiling the 2025 Chevrolet Equinox – Where Style Meets Versatility

Unveiling the 2025 Chevrolet Equinox – Where Style Meets Versatility

{kind=link}